客服热线:

客服热线:

By Bryce Coward

This week’s breakout in gold is an epic expression of our times in which potential economic problems are quickly followed by massive actual and expected responses by central banks and governments. The problem de jour (for both markets and the public) is of course the real and scary health and economic consequences of a further spread COVID-19. So far, gold has been a beneficiary of the market’s response to the slowing growth prospects brought by the virus. We’ll explain why below.

上周金价的向上破位昭示了一点,如果经济出现大问题,各国政府和央行会迅速地采取实际的或预期将采取力度相当大的应对举措。当前市场和公众所共同面临的问题当然是新冠疫情的进一步蔓延会在公共卫生以及经济方面实际带来的可怕后果。到目前为止,市场对疫情导致的经济增速放缓的反应让黄金成了大赢家,原因解读如下。

But before we get to that, it may be useful to take a step back and examine how the gold price has evolved both in nominal terms and relative to stocks. As we can see in the chart below, it doesn’t take a master technical chartist to see that the price of gold stopped going down in 2015, went sideways from 2015-2019 and then “broke out” of two major resistance levels. The first such resistance level was $1300/oz, which was broken back in the middle of 2019. The second one was $1600/oz, which was broken this week.

但在此之前,有必要先回顾一下金价在绝对涨幅以及相对于美股回报方面的表现。如下图所示,即便不是技术分析方面的高手也能看清楚金价在2015年止跌,在2015-2019年期间横盘整理,随后突破了两个重要的阻力位。第一个阻力位在1300美元,于2019年中被冲破,第二个阻力位就是在上周被突破的1600美元。

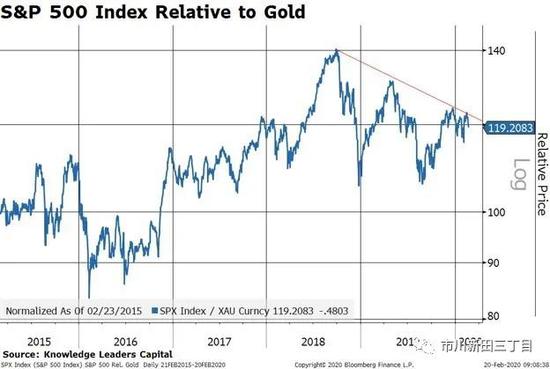

In this second chart, we see that the S P 500 has slowly started to underperform the barbaric relic beginning in late-2018 despite the S P 500 having risen by 15% over that time frame.

下图显示,标准普尔500指数的涨幅开始落后于黄金的趋势始于2018年末,尽管自那时至今标准普尔500指数上涨了15%。

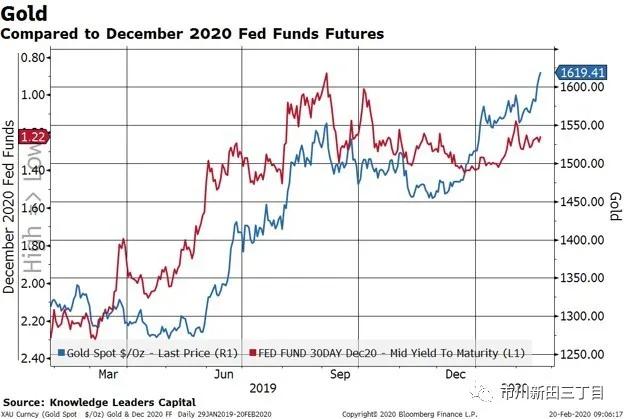

What changed in late-2018 to start this trend of gold’s positive nominal and relative performance? Central bank intervention of course, and the inexorable crushing of real interest rates. Since 2018 the Fed has stopped quantitative tightening, cut the Fed Funds rate 3 times and started a “not-QE”. Currently, market participants are expecting two more rate cuts by the end of the year. And this when stocks are at all-time highs. If the stock market were to correct even by 5% or 10%, how many rate cuts would the market expect/demand then?

在2018年末是什么东西发生了变化从而导致金价无论是从价格的绝对波幅乃至相对表现方面均如此突出?央行的干预当然是其中一个因素,还有就是实际利率的水平在势不可挡地下行。自从美联储在2018年终止量化紧缩以来,已连续三次调降了联邦基金的利率并开启了“嘴上不承认,身体很诚实”的量化宽松。当前,市场人士预测在今年年底前还会降息两次,这还是在美股创新高的情况下。如果美国股市调整个5%或10%,市场所期盼的或要求的降息次数又将是多少呢?

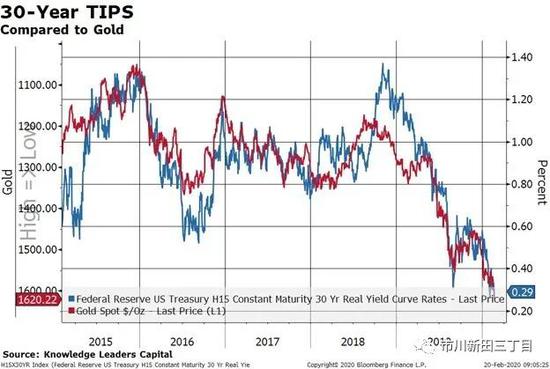

These expectations are pushing inflation-adjusted rates, proxied here by 30Y TIPS yields, to new cycle lows. Real rates are inversely correlated with the price of gold, hence cycle highs in gold.

这些预期正在将以30年期通胀保值美国国债的收益率为代表的通胀调整后的美国实际利率的水平推至本轮经济周期的新低,实际利率的水平与金价负相关,因此在金价上涨的时期实际利率的水平会处于低位。

在下面第一张图中,左轴为根据2020年12月份交割的联邦基金利率期货合约的报价推导出的联邦基金利率的水平,指标是倒过来表示的,越往下联邦基金利率的水平越高;右轴为正常表示的金价。

下面第二张图中,左轴为倒过来表示的金价;右轴为30年期通胀保值美国国债的收益率。

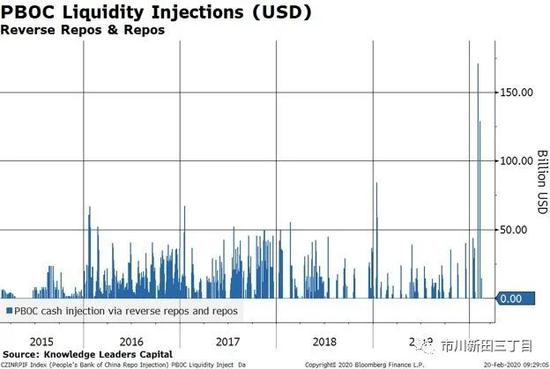

But the thing is that it’s not just the Fed that is stepping in to push real rates lower. The other elephant in the room is China, which is completing both monetary and fiscal stimulus to counteract the virus’s economic fallout. In the next chart I show the PBOC’s liquidity injections via reverse repurchase agreements with banks and other financial intermediaries. In a reverse repo agreement, a bank would exchange its less-liquid collateral for cash from the central bank for a set time period. In this way, the central bank can make the financial system more liquid for a time. Over the last few weeks, the PBOC’s liquidity injections have dwarfed anything previously seen.

但正忙着推低利率水平的可并不仅仅是美联储。另一个不容忽视的因素来自中国,中国正在货币政策和财政政策两方面双管齐下以应对疫情给经济带来的恶果。下图显示的是中国人民银行通过逆回购向商业银行和其他金融机构提供流动性的情况,在逆回购交易中一家商业银行向央行提供流动性不那么好的金融资产作为抵押并获得一段时间的资金融通。通过这种方式,央行可以让金融体系暂时处于流动性较充裕的状态,中国人民银行过去几个星期的流动性注入规模达到了前所未有的程度。

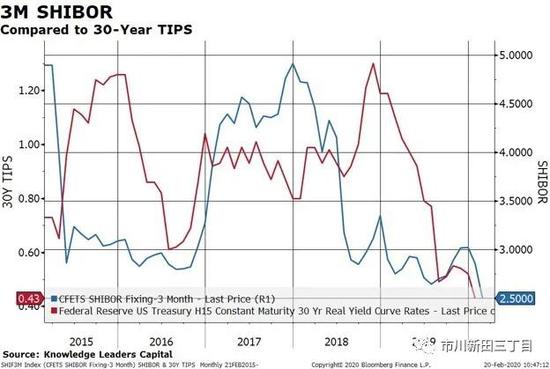

In turn, lending rates between Chinese banks – proxied by the Shanghai Interbank Offered Rate – have crashed to new lows. This sounds like a good thing, and it normally is a sign of a well-functioning financial system. However, far from being a sign of easy financial conditions, what SHIBOR rates are really telling us at this juncture is that the Chinese government is overwhelming the financial system with cash to try to prevent a meltdown. This is why SHIBOR rates, once uncorrelated with TIPS and gold, are now helping to drive real rates lower and gold higher.

继而,以上海银行间拆借利率SHIBOR为代表的中国各家商业银行之间的融资成本也降至历史新低。听上去挺不错,在正常情况下这意味着金融体系运作良好。但在当前这个节点,这可不是融资状况比较宽松的迹象,SHIBOR的水平真正揭示的是中国政府正在向金融体系大举放水以防止市场崩溃,这就是为什么以前与金价和通胀保值美国国债的收益率并不相关的SHIBOR如今也在拉低实际利率的水平和拉高金价方面发挥作用的原因了。

新浪财经公众号

24小时滚动播报最新的财经资讯和视频,更多粉丝福利扫描二维码关注(sinafinance)